In cross-border wealth management and estate planning for high-net-worth individuals, trusts are often used for risk isolation, managing distribution pacing, and family governance. However, there is still a gap in market understanding, with trusts sometimes misunderstood as making assets "invisible" or information "completely isolated."

In essence, a trust is a legally enforceable and supervised relationship established through contracts and legal frameworks, enabling assets to be managed, utilized, and transferred in a predictable manner, even across generations, international borders, and high-risk scenarios.

So-calledOffshore TrustThis typically involves establishing the trust in an offshore jurisdiction, with its governing law, trustee, or management operations located in an offshore legal domain (commonly in common law jurisdictions like the UK or US, or specific trust-friendly jurisdictions), to achieve cross-border asset governance objectives through its institutional tools.

1. Core Structure of a Trust: Three Parties, Two Relationships, and Three Major Certainties

The key to understanding trusts is not memorizing clauses, but grasping how "rights, obligations, and control" are arranged and distributed.

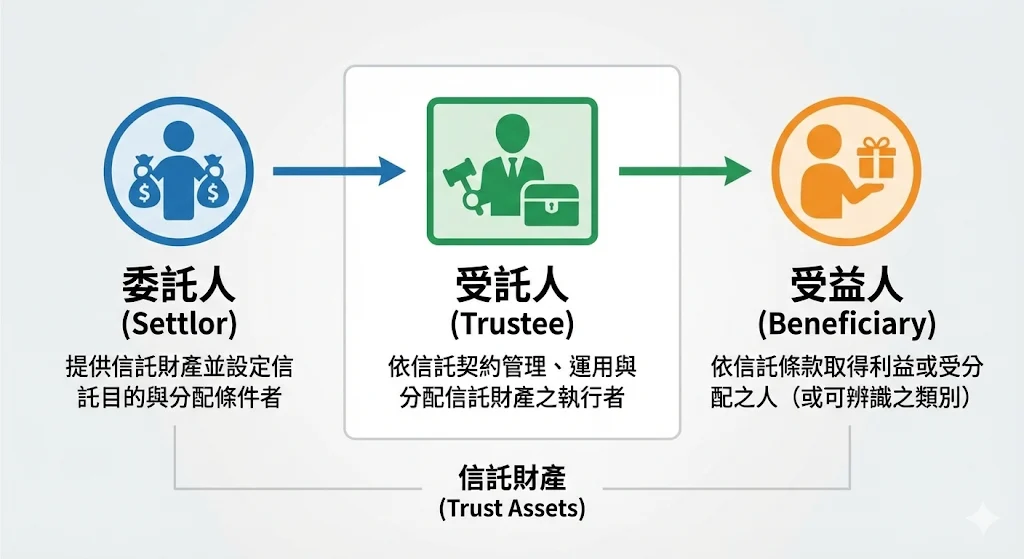

Three Parties

- SettlorProvider of trust property and setter of trust purposes and distribution conditions

- TrusteeThe executor who manages, utilizes, and distributes trust property according to the trust agreement.

- BeneficiaryBeneficiary (or identifiable class of beneficiaries) of a trust

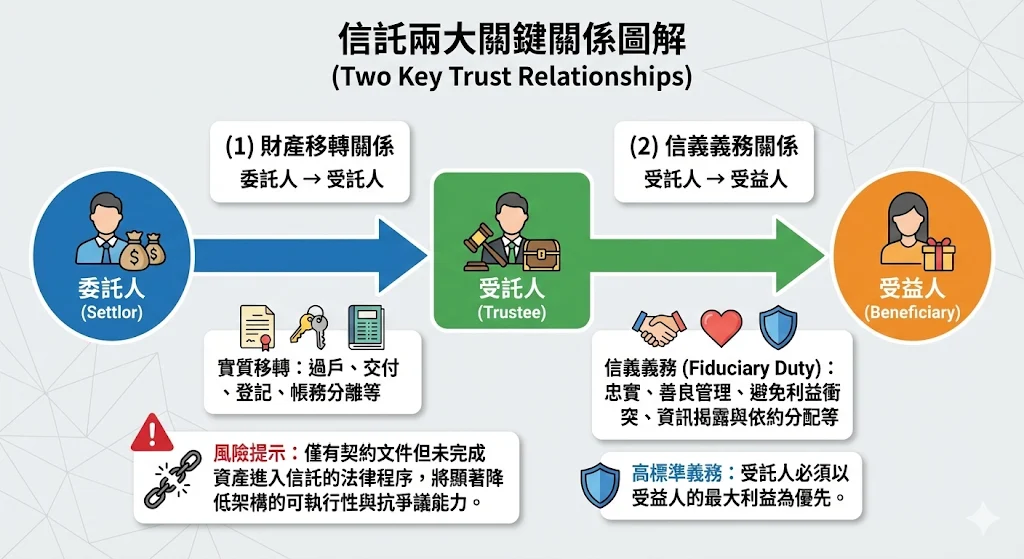

Two Key Relationships

relationships

Property transfer relationship: Trustor → Trustee

Whether a trust can be established and remain valid often first depends on whether the trust property has been completed.Substantive transfer(transfer, delivery, registration, or book-entry segregation, etc.). Merely having the contractual documents without completing the legal procedures for the asset to enter the trust will significantly reduce the executability and dispute resilience of the structure.

Fiduciary Relationship: Trustee → Beneficiary

When a trustee obtains the right to manage and dispose of assets, they simultaneously assume fiduciary duties towards the beneficiaries. These duties include requirements for loyalty, diligent management, avoidance of conflicts of interest, disclosure of information, and distribution according to the trust agreement. If the trustee is merely a nominal holder and the trust is practically operated entirely under the settlor's direction, it may weaken the legal robustness and asset isolation effect of the trust.

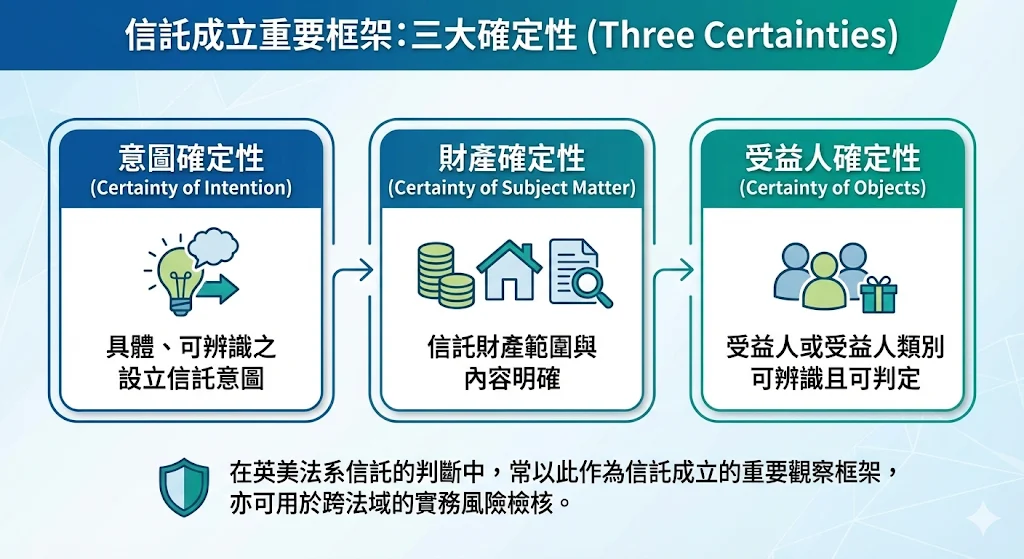

3) Three Certainties

In the judgment of trusts in Anglo-American legal systems, the "three certainties" are often used as an important framework for observing the establishment of a trust, and can also be used for practical risk assessment across different legal jurisdictions:

- Certainty of IntentionSpecific, identifiable intention to establish a trust

- Certainty of Subject Matter:Scope and content of trust property are clear

- Certainty of ObjectsBeneficiary or class of beneficiaries are identifiable and determinable

If any of the above requirements are unclear, the trust's defense against legal challenges (creditor claims, tax assessments, family disputes) will be significantly weakened.

II. Domestic Trusts vs. Offshore Trusts: Key Differences Lie in Legal Design and Governance Tools

A common customer question is, "Taiwan already has a Trust Law, so why is an offshore trust still needed?" In practice, the differences are mostly not in "location," but rather inInstitutional flexibility, cross-border integration capabilities, and completeness of governance tools。

1) Structural differences between ownership and equity

The typical characteristic of a trust in common law systems is the dissection of the concept of ownership into:

- Legal TitleHeld by multiple trustees for management, disposition, and external actions.

- Equitable InterestHeld by the beneficiary, used to assert trust interests and beneficiary rights

This structure typically offers greater flexibility in terms of clause design, beneficiary rights arrangements, distribution discretion, and protective mechanisms (such as protector systems).

2) Effects and Limitations of Asset Segregation

Trusts are often used for asset isolation, but it must be emphasized that the isolation effectnot equivalent toExemption from existing debts or improper transfers. Most jurisdictions have provisions for the revocation or denial of fraudulent transfers or improper transfers; if the purpose and timing of the trust's establishment are unfavorable to creditors, the structure may be challenged.

3) CRS and Information Transparency: Replacing "Invisible" Imaginings with Compliant Governance

In an environment where CRS and cross-border information exchange are normalized, the feasibility of offshore arrangements depends onExplainability and regulatory complianceFinancial institutions' KYC/AML due diligence requires stricter identification of relevant parties in trust structures (settlors, trustees, beneficiaries, protectors, etc.). Therefore, offshore trusts should be positioned as "cross-border governance and compliance management tools," rather than information isolation tools.

III. Four Common Trust Structures in Practice (Choosing by Need)

Lifetime Interest Trust

A enjoys lifetime benefits, and the remaining property after A's death goes to B. Commonly used to balance care obligations with the designation of final ownership.

Contingent Interest Trust

Beneficiaries must meet certain conditions (age, education, succession assessment, etc.) to receive benefits, which are used for controlling the distribution rhythm and preventing premature asset concentration.

3) Discretionary Trust

The trustee distributes at a time, to a recipient, and in an amount determined by their discretion under the authorization. This type typically relies more heavily on the quality of trustee governance and document design, but often exhibits higher resilience in equity arrangements.

Protective Trust

When beneficiaries face events such as bankruptcy, debt, or marital risk, the terms can activate protective mechanisms (e.g., adjusting payment conditions or converting distribution models) to reduce the possibility of assets being accessed by external parties.

IV. Tax and Compliance Priorities for 2026: CFCs and Ongoing Maintenance Costs

Since the implementation of Taiwan's CFC (Controlled Foreign Company) system (starting in 2023), trust arrangements involving offshore holdings, offshore company equity, or cross-border investment vehicles should be included in CFC risk assessment and reporting planning. Even without actual profit distribution, specific tax and reporting obligations may be involved, requiring more comprehensive documentation and ongoing maintenance.

In this context, a more reasonable positioning for offshore trusts is to manage tax and information transparency requirements in a institutionalized manner, enabling the structure to operate in a compliant and well-governed way long-term.

5. Common Failure Scenarios and Control Points: Control Rights Configuration and Document Consistency

In trust planning, the most common structural weakness is often not in the terms themselves, but rather inExcessive concentration of controlThe client wishes to maintain a high degree of control while achieving maximum isolation.

However, under the legal logic of most jurisdictions, the degree of control retained and the effectiveness of asset isolation often have an inverse relationship. If the settlor retains too much control, effectively being able to direct the operation of the assets at any time, the structure may be questioned as a mere formality in the event of a dispute, thereby weakening its overall protective power.

Therefore, sophisticated trust arrangements typically focus on:

- Clear objectives and reasonable power distribution

- Document Consistency and Auditability

- Integrated with tax/compliance planning

- Long-term governance and maintenance mechanisms (rather than one-time establishment)

The value of offshore trusts lies in their "operable governance structure."

Offshore trusts are not informational silos, but rather institutionalized arrangements for cross-border governance and inheritance. In an environment where CRS, CFC, and compliance costs have become the norm, frameworks that can be established and operate effectively long-term are often not the most complex, but rather the most consistent, explainable, and executable.

This article is for general informational and conceptual purposes only and does not constitute legal, tax, or investment advice. Actual planning requires comprehensive assessment based on the client's/beneficiary's tax residency, asset types, ownership structure, and relevant legal jurisdiction regulations.

If you are evaluating the suitability of offshore trusts for cross-border asset allocation, family inheritance, or shareholding structures (including CFC implications), we can provide an initial diagnosis and feasibility assessment. This will help you establish a long-term, operable asset governance solution in compliance with regulations.